Brilliant founders are discovering that their postal code determines their valuation more than their product

In 2024, Latin American startups attracted around $4.2 billion in venture capital, and the region now boasts around thirty unicorns compared to just nine in 2019. Yet beneath these impressive headlines lies a more fascinating story: the importance of geographic arbitrage in the global startup ecosystem.

Valuation Disparities

Consider this statistical anomaly: LATAM startups with similar product-market fit, revenue profiles, and growth trajectories consistently trade at lower revenue multiples in their home markets as compared to U.S. companies. This isn’t market inefficiency—it’s systematic mispricing that has created a valuation gap of billions across the region’s top growth-stage companies.

The structural challenges run deeper than simple valuation gaps. Early-stage funding in LATAM remains limited, highly concentrated, and burdened by regional risk premiums that depress valuations regardless of company quality. Many promising startups struggle to raise meaningful capital, access sophisticated financial infrastructure, or position themselves for high value exits. These companies often remain heavily exposed to regional volatility, creating additional friction that compounds their disadvantages.

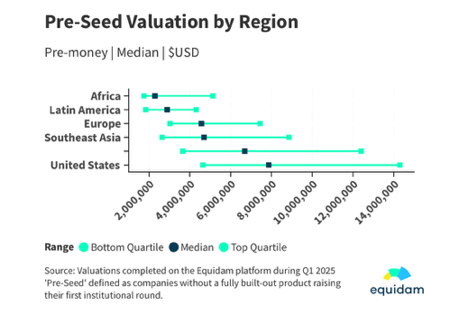

The numbers tell the story of structural disparity. While LATAM’s venture capital ecosystem manages $12.4 billion in dry powder, the U.S. market sits on $580 billion—a 47x difference that translates directly into founder outcomes. Regarding valuations, U.S. startups at the seed and Series B stages raise larger rounds and command higher valuations than any other region globally.

Strategic Migration

What’s emerging isn’t brain drain, but something far more sophisticated: geographic arbitrage optimization. An increasing percentage of LATAM unicorns and start-ups now maintain significant U.S. operations, not as an escape from their home markets but as a multiplier for their regional advantages.

A gateway not just to capital, but to a model where they can buy global scale at regional efficiency prices. It’s a strategic code these entrepreneurs have cracked.

Take Nowports, the Monterrey-based logistics platform founded in 2018. When CEO Alfonso de los Ríos opened a Miami office in 2023, he wasn’t just establishing a logistical foothold in a major US port—he was repositioning his entire company for capital access and building the foundation to facilitate a robust vertical integration model offering insurance and financing. The result was a $240 million funding round across Series A, B, and C rounds led by SoftBank, Tiger Global, Foundation Capital, and others, at 4.2x valuations. As de los Ríos observed, “Miami didn’t just give us port access—it gave us investor access.”

This pattern repeats across sectors. Mexican fintech Broxel, founded in 2011 as an app for streamlining multiple currency accounts for remittances, discovered that establishing offices in Texas and California—strategic locations in the remittance industry—opened new customer segments. When the company launched its Miami Dolphins-branded prepaid card through a Miami office alliance, it wasn’t just a marketing gimmick but a strategic embedding that elevated its brand across North America.

Four Pillars of Arbitrage

The migration northward is based on four strategic foundations that collectively create an irresistible pull for ambitious founders in LATAM.

- Capital density remains the primary driver. Despite LATAM’s maturing venture ecosystem, 55.5% of global venture capital assets under management remain U.S.-based. The depth, scale, and diversity of the U.S. investment landscape simply cannot be replicated in regional markets. While venture capital activity in Latin America has grown significantly over the past decade, early-stage funding remains limited and highly concentrated, often requiring companies to accept lower valuations due to perceived regional risk.

Institutional investors still allocate domestically first, creating a natural ceiling for LATAM-only startups that U.S. presence immediately lifts. The U.S. offers access to vast networks of capital firms, corporate investors, and growth equity funds that actively seek exposure to high-growth sectors, such as fintech, logistics, and healthcare, precisely where LATAM startups have been thriving. - Market unification offers a second compelling advantage. While LATAM encompasses 660 million people across 33 countries with distinct currencies and regulatory frameworks—markets that remain fragmented by language, regulations, and economic volatility—the U.S. presents 330 million consumers operating within a single currency, regulatory system, and logistics infrastructure. More crucially, the average U.S. household income is $61, 984 USD. Compare that to Costa Rica, the country leading in average income in LATAM, with an average income of $1,045 USD, creating premium customer segments that justify higher unit economics.

The U.S. market offers unmatched scale, purchasing power, and infrastructure, enabling companies to test new products, capture premium customers, and establish brand recognition in a globally visible space. Success in the U.S. validates business models and increases attractiveness to future investors in ways that fragmented regional success cannot match. - Financial infrastructure provides the operational backbone that fragmented LATAM systems often cannot. While Latin America’s financial systems have improved in recent years, challenges such as regulatory restrictions, currency volatility, and limited venture debt markets create significant barriers for startups seeking to scale rapidly or manage cross-border operations.

The U.S. banking ecosystem offers several critical advantages: stable financial services, access to venture debt and growing financing products not widely available in LATAM, advanced digital payment processing services, and easier integration with global financial markets. For startups managing international customer bases, U.S. operations simplify the collection of U.S. dollar revenues, payments to suppliers, and the establishment of partnerships with major financial institutions.

That fluency often takes shape through financial infrastructure, where U.S.-based systems become not just a convenience but a competitive advantage.

Meanwhile, Uruguayan API company Prometeo, founded in 2018, exemplifies this infrastructure advantage. The company entered the U.S. market in June 2024 with a Bank Account Validation API connecting Latin American businesses to 100% of U.S. banks via a single integration. By March 2025, Prometeo had expanded to a full “Borderless Banking” suite, enabling companies to open accounts for collections, automate payments, and track fund movement across U.S. and Latin American banking systems. This U.S. integration became a product advantage rather than merely an operational necessity, enabling clients to conduct secure, compliant financial operations essential for scaling cross-border services while attracting top-tier investors. - Exit optimization closes the loop on value creation. There have been 79 venture capital-backed startup exits in Latin America since 2017, however the number has been declining since 2021 suggesting that a significant portion of exits may have involved U.S. acquirers or IPOs.

Cornershop’s $3 billion acquisition by Uber exemplified this dynamic—the Chilean-Mexican company’s early U.S. establishment made it an ideal integration target, enabling an exit that might have been capped at a fraction of the exit amount without American operational presence.

Cost of Migration

This arbitrage opportunity comes at a cost. Execution complexity multiplies as companies navigate dual compliance regimes, cultural gaps, and visa constraints for key talent. Customer acquisition costs can rise significantly as companies recalibrate their messaging and distribution for new markets. Operational overhead can increase by hundreds of thousands of dollars annually due to the costs of managing legal, tax, and compliance requirements across multiple jurisdictions. A study done on 68 fintech companies in LATAM found that costs tend to increase by 10% when expanding into markets like Mexico, Uruguay, Colombia, and Chile.

Perhaps most significantly, the strategy requires founders to maintain a delicate balance between global ambition and regional roots. The most successful practitioners aren’t abandoning LATAM but leveraging it, keeping R&D, engineering, and core operations in cost-efficient home markets while establishing strategic footholds in higher-value ecosystems.

Opportunistic Geographic Arbitrage

The Latin American startup ecosystem has become one of the world’s most dynamic markets, capturing increasing attention from U.S. investors, venture funds, and strategic buyers. Yet, while LATAM offers exceptional energy, talent, and market opportunity, the structural constraints remain real. Limited capital pools, fragmented consumer markets, and constrained exit routes all pose challenges for startups operating solely within regional boundaries. To mitigate against these constraints, establishing operations or legal entities in the United States provides access to advantages that are difficult to replicate in Latin America.

This isn’t about abandoning LATAM markets—it’s about building the financial and operational foundation necessary to compete and thrive on a global stage. In an era where digital infrastructure has theoretically flattened global competition, these entrepreneurs are demonstrating that physical presence and strategic positioning still generate significant value. And what’s unfolding across Latin America represents the emergence of a model for global startup development that challenges Silicon Valley’s monopoly on innovation scaling. These founders are proving that world-class companies can be built anywhere but optimized everywhere, recognizing that geography is not a destiny, but a strategic advantage.

For investors, this creates opportunity: backing top-tier talent at regional prices with global upside potential.

Macaluso LLP LATAM Team:

Michael Macaluso

[email protected]

Peter Cejas

[email protected]

Todd Vollmers

[email protected]

Jack Cahill (tax)

[email protected]

Tom Kennedy (regulatory)

[email protected]